Group Management Report Products Safety and Health Environment Human Resources Social Commitment Consolidated Financial Statements 61

liabilities, which sank in the course of the corporate tax

reform in the U.S. The share of total non-current debt

dropped from 18 % to 15 %. The amount of current debt

on the balance sheet increased from € 407.5 million to

€ 446.9 million on December 31, 2017. This development

was due to the expansion of liabilities from trade accounts

payable on account of the expansion of business activity

and the increase in current debt in the course of the re-

classification of the promissory note tranches due in 2018

(€ 64 million).

The net financial debt, comprising the balance of cash

and cash equivalents, short-term financial assets, current

marketable securities, loans granted, debt, and employee

benefit obligations, reached € 78.0 million at the end of

2017, after net financial assets of € 25.7 million were dis-

closed in the previous year.

Principles and Goals of Our Financing Strategy

We generally aim to finance our operating business activities

from the cash flow from operating activities. The same

applies to the need for capital expenditure, which caters to

the continual expansion of business activities.

As a result, our financing strategy is oriented to keeping

the cash and cash equivalents generated within the Group

centralized. In addition, a financing framework is sought that

enables ALTANA to flexibly and quickly carry out acquisi-

tions and even large investment projects beyond the accus-

tomed scope.

To successfully implement these goals, we manage nearly

all of the Group’s internal financing centrally via ALTANA AG.

To this end, cash pools are set up for all of the important cur-

rency areas.

At the end of 2017, ALTANA’s liabilities totaled € 192 mil-

lion due to the issuance of two promissory note loans in

2012 and 2013 (€ 350 million in total). The outstanding prom-

issory note loans are divided into tranches with fixed inter-

est rates and different maturities. The loans will be repaid by

2020. Furthermore, there is a general syndicated credit

facility of € 250 million. The term of this credit facility will last

until 2022.

This financing structure offers ALTANA the flexibility it

needs to appropriately take advantage of short-term or

investment-intensive growth opportunities. The distribution

of the maturities of the financing instruments we use en-

ables us to optimally control repayment of liabilities with in-

flows from operating cash flow.

We continue to use off-balance-sheet financing instruments

to a very limited extent. These include purchasing

commitments, operating leasing commitments, and guarantees

for pension plans. Details on the existing financing

instruments are provided in the online Consolidated Financial

Statements.

Liquidity Analysis

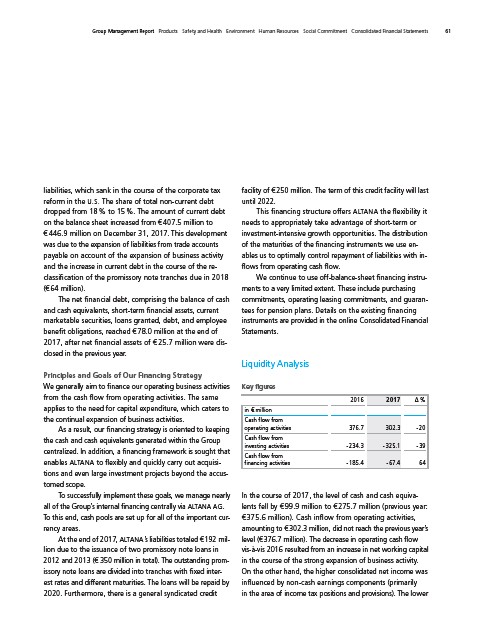

Key figures

2016 2017 Δ %

in € million

Cash flow from

operating activities 376.7 302.3 - 20

Cash flow from

investing activities - 234.3 - 325.1 - 39

Cash flow from

financing activities - 185.4 - 67.4 64

In the course of 2017, the level of cash and cash equiva-

lents fell by € 99.9 million to € 275.7 million (previous year:

€ 375.6 million). Cash inflow from operating activities,

amounting to € 302.3 million, did not reach the previous year’s

level (€ 376.7 million). The decrease in operating cash flow

vis-à-vis 2016 resulted from an increase in net working capital

in the course of the strong expansion of business activity.

On the other hand, the higher consolidated net income was

influenced by non-cash earnings components (primarily

in the area of income tax positions and provisions). The lower