Letter from the Management Board | About This Report | Sustainability Management | Corporate Bodies and Management | Report of the Supervisory Board | Shaping the Future Together | Group Management Report | Products | Safety and Health | Environment | People | Social Commitment | Consolidated Financial Statements (condensed version) | Multi-Year Overview | Global Compact: Communication on Progress (COP) | ALTANA worldwide | List of Shareholdings | Overview | Contact

General Business Setting

Overall Economic Situation

The global economy as a whole faced considerable challenges in 2022, leading to a general slowdown in the markets. Following global growth of 6.2 % in the previous year, which was characterized by exceptionally high demand, the International Monetary Fund (IMF) currently estimates that global economic output will increase by only 3.4 % in 2022. The most influential event in 2022 was certainly the start of Russia’s war against Ukraine in February. Apart from the humanitarian catastrophe this event triggered, the economic impact was felt around the world. There was a further increase in commodity prices, which were already at a very high level at the beginning of the war. At the same time, energy prices rose significantly and, especially in Europe, had a negative impact on the macroeconomic development. Regarding natural gas, there was a risk of shortages in Europe due to suspended or greatly reduced supplies from Russia. Worldwide inflation rose to levels not seen for decades. In addition, the coronavirus pandemic continued to weigh on economic development in 2022: While in many countries no further significant restrictions on economic activity were deemed necessary to combat the pandemic, the strict zerocovid policy adhered to by the Chinese government for most of the year led to ongoing disruptions to supply chains and a decline in Chinese economic growth, which impacted global economic performance.

According to IMF estimates, the Eurozone achieved 3.5 % growth in 2022. The economic upturn of the previous year (5.3 %) was weakened overall since the beginning of 2022 by the enormous political and economic challenges. This affected all major markets, albeit to varying degrees, with the dependence on Russian natural gas supplies among the factors influencing the economic slowdown. According to IMF estimates, economic output in Germany grew by 1.9 % (previous year: 2.6 %). In other Eurozone markets, growth remained at a somewhat higher level, for example in Italy at 3.9 % and Spain at 5.2 %.

The IMF currently estimates that the economies of the Americas developed slightly positively overall in 2022, although here, too, at a comparatively low level due to high inflation. The IMF estimates that the U.S. achieved growth in gross value added of 2.0 %, while Canada was expected to grow by 3.5 %. In the Latin American countries, growth totaled 3.9 %, weakening overall compared with the previous year. According to IMF estimates, Brazil achieved growth of 3.1 %, showing the same trend.

Based on IMF assessments, Asia was also able to achieve an overall increase in gross domestic product in 2022, but here, too, with varying intensity. China, which posted growth of 8.4 % in the previous year, was only able to close 2022 with a growth rate of 3.0 %. India, which grew by 8.7 % in the previous year, largely maintained momentum and achieved a 6.8 % increase in gross value added according to IMF assessments. The countries of the ASEAN 5 group also achieved a solid growth rate of 5.2 % overall, following an increase of 3.8 % in the previous year. Japan, with growth of only 1.4 %, was even below the low level of the previous year.

Industry-Specific Framework Conditions

The American Chemistry Council (ACC) estimates that global chemical production grew by 2.0 % in the past fiscal year (previous year: 5.2 %). As a result, the development of the chemical industry was slightly below the overall economic growth of 2022, which can be explained, among other things, by the high dependence of chemical production on fossil energy sources. There were major regional differences in this respect. While the Americas were able to draw on their own resources, in Europe, and especially in Germany, the strong dependence on Russian natural gas was noticeable.

According to estimates by the German Chemical Industry Association (VCI), Germany, Europe’s largest chemical producer, recorded a decline (- 6.0 %) for the industry as a whole. Excluding the share of the pharmaceutical sector, the VCI even expects a 10.5 % decrease for the past fiscal year. In other Eurozone countries, such as Italy (VCI: - 3.3 %) and France (VCI: - 2.9 %), declines were also recorded, although not to the same extent. In the United Kingdom, the chemical industry also showed declining figures (VCI: - 4.1 %). Overall, according to the ACC, the industry in Western Europe developed far below the global average at - 3.2 %. In Eastern Europe (including Russia), the situation was far worse overall, at - 7.3 %, due to the economic impact of the war against Ukraine.

The ACC estimates that chemical production in the United States increased by 3.9 % overall. The above-average development of the U.S. chemical industry, also in comparison to the overall economic development, was due on the one hand to high demand. In addition, the country’s greater independence in the energy sector – especially with regard to natural gas – caused less uncertainty than in Europe. In Latin America, the sector developed somewhat more weakly than in North America, with overall growth of 2.6 %.

According to the ACC, the chemical industry in the Asia-Pacific region recorded growth of 2.7 % in fiscal 2022. In contrast to the overall economic development, China, the largest producer in the industry, outperformed the average development of the region with growth of 6.0 % (VCI). India achieved solid growth of 4.6 % (VCI). By contrast, the chemical industry in Japan declined by 2.9 % (VCI) and in South Korea by 6.8 % (VCI).

After a demand-driven sharp rise in oil prices in 2021, the markets were expected to stabilize at a high level in 2022. But Russia’s war against Ukraine fundamentally changed the situation on the energy markets and the price of a barrel of Brent crude oil rose to a high of 123 U.S. dollars (June 2022) during the first few months of the war, before gradually falling back to 81 U.S. dollars by the end of the year. The average price for the year (101 U.S. dollars) was thus significantly higher than the previous year’s level (71 U.S. dollars).

Important Events for Business Development

In 2022, non-operating effects at ALTANA influenced the company’s earnings and financial position as well as its assets.

Non-operating effects from acquisitions in the 2022 fiscal year resulted exclusively from transactions already completed in the previous year by ECKART (acquisition of the business of TLS Technik GmbH & Co. Spezialpulver KG in Bitterfeld in February 2021) and ACTEGA (acquisition of Henkel’s closure materials business in May 2021).

The development of the exchange rates between the euro, the Group currency, and other currencies important for ALTANA had a positive impact on sales and earnings in 2022. The exchange rate of the euro to the U.S. dollar had the greatest effect in 2022. At an average of 1.05 U.S. dollars for one euro, it was lower than in the previous year (1.18 U.S. dollars for one euro). Further significant positive effects from changed exchange-rate relations resulted from the rate of the Chinese renminbi to the euro, which at 7.08 CNY for one euro was also lower than in the previous year (7.63 CNY for one euro), and the rate of the Brazilian real, which at 5.44 BRL for one euro was significantly lower than in the previous year (6.38 BRL for one euro). By contrast, the average exchange rate of the euro to the Japanese yen rose from 129.88 JPY for one euro to 138.03 JPY for one euro in 2022, leading to corresponding negative effects. In addition, differences in exchange rates on the balance sheet date had a net increasing effect on balance sheet items compared to the previous year.

Business Performance

Group Sales Performance

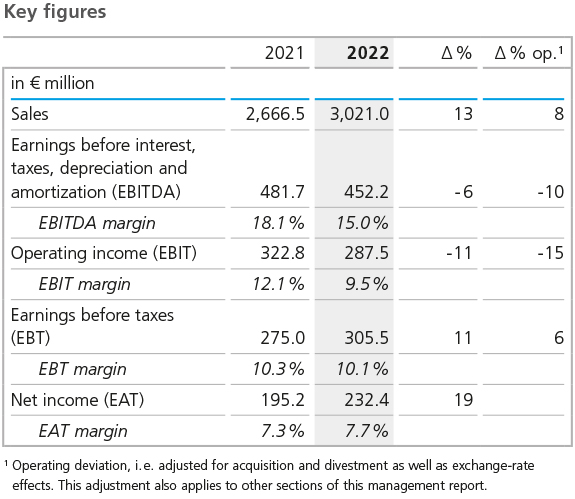

Despite a highly volatile and challenging environment, Group sales exceeded the € 3 billion threshold for the first time in 2022, reaching a total of € 3,021.0 million. Sales thus increased by 13 % or € 354.5 million compared to the previous year (€ 2,666.5 million). Non-operating effects had in total a positive impact on sales development. The aforementioned exchange-rate changes resulted in a significant increase in sales of € 138.6 million or 5 %. Acquisitions increased sales by a total of € 10.4 million, primarily due to the ACTEGA division’s acquisition of Henkel’s closure materials business (€ 9.8 million), which was already completed in 2021, but also as a result of the business activities of TLS Technik GmbH & Co. Spezialpulver KG in Bitterfeld, Germany, which was acquired also in 2021 by ECKART. Adjusted for exchangerate and acquisition effects, sales were 8 % above the prior-year figure.

The start of Russia’s war against Ukraine in February 2022 accelerated the decline in demand on the part of our customers over the course of the year and consequently led to noticeable volume losses. Our decision not to supply any of our products to Russia or Belarus as of March 2022 until further notice, even in cases where this would have been permissible under the sanctions adopted, led to additional losses. Another influencing factor, especially regarding the regional development of our sales, was the slackening demand in China, which had a noticeable impact on the local sales volume and sales development. Overall, ALTANA exceeded the sales growth forecast for 2022 despite the drop in volumes, boosted by extensive price adjustments as a result of sharp price increases for raw materials, energy, and logistics services. At the beginning of the year, we had expected mid-single-digit percentage growth.

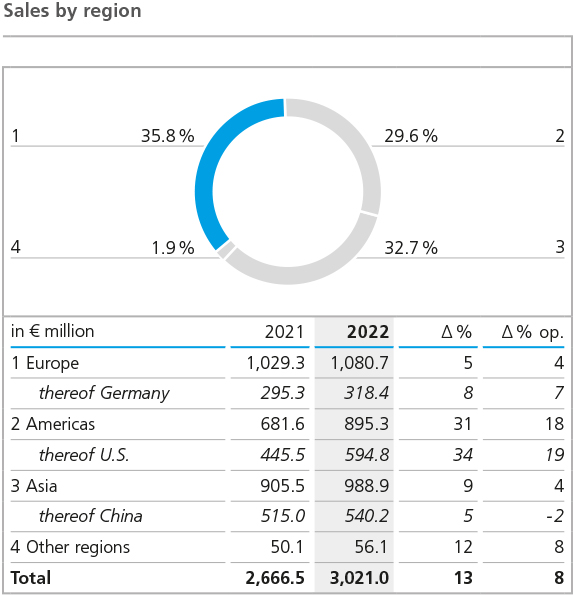

On account of the changed framework conditions, there were shifts in the regional sales structure. Accounting for a share of 36 % of total Group sales (previous year: 39 %), Europe continued to be ALTANA’s most important sales region, but at the same time was hit hardest by the economic effects of the war against Ukraine. The loss of the Russian and Belarusian markets resulted in sales losses amounting to approximately € 38 million. The comparatively low European growth of 5 %, or 4 % when adjusted for acquisitions and exchange-rate effects, reflects the general clouding of the markets.

In 2022, sales in the Americas were 31 % up on the previous year. Adjusted for significantly positive exchange-rate effects, operating growth amounted to 18 %. Operating sales in the United States increased by 19 %. The share of total Group sales rose to 20 % in 2022 (previous year: 17 %), with the U.S. once again becoming the Group’s strongest market in terms of sales. Growth rates were also in double digits in almost all of the other countries in the Americas. Mexico achieved operating growth of 17 %, followed by Brazil and Canada. The Americas’ share of Group sales climbed to 30 % in 2022 (previous year: 26 %) as a result of the overall positive development.

In the past fiscal year, Asia’s share of total Group sales declined slightly from 34 % to 33 %. Nominal sales growth in the region was 9 %, while operating growth, adjusted mainly for positive exchange-rate effects, was 4 %. The driver of growth in this region in 2022 was India, which achieved the Group’s highest overall growth rate with a very dynamic sales development and operating growth of 27 %. The Middle Eastern countries and Southeast Asia also recorded significant double-digit operating sales growth. Slowing demand in China, the region’s largest single sales market, led to a 2 % decrease in operating sales. The share of this market in the Group’s total sales fell from 19 % to 18 %.

In 2022, sales in the Americas were 31 % up on the previous year. Adjusted for significantly positive exchange-rate effects, operating growth amounted to 18 %. Operating sales in the United States increased by 19 %. The share of total Group sales rose to 20 % in 2022 (previous year: 17 %), with the U.S. once again becoming the Group’s strongest market in terms of sales. Growth rates were also in double digits in almost all of the other countries in the Americas. Mexico achieved operating growth of 17 %, followed by Brazil and Canada. The Americas’ share of Group sales climbed to 30 % in 2022 (previous year: 26 %) as a result of the overall positive development. In the past fiscal year, Asia’s share of total Group sales declined slightly from 34 % to 33 %. Nominal sales growth in the region was 9 %, while operating growth, adjusted mainly for positive exchange-rate effects, was 4 %. The driver of growth in this region in 2022 was India, which achieved the Group’s highest overall growth rate with a very dynamic sales development and operating growth of 27 %. The Middle Eastern countries and Southeast Asia also recorded significant double-digit operating sales growth. Slowing demand in China, the region’s largest single sales market, led to a 2 % decrease in operating sales. The share of this market in the Group’s total sales fell from 19 % to 18 %.

Sales Performance of BYK

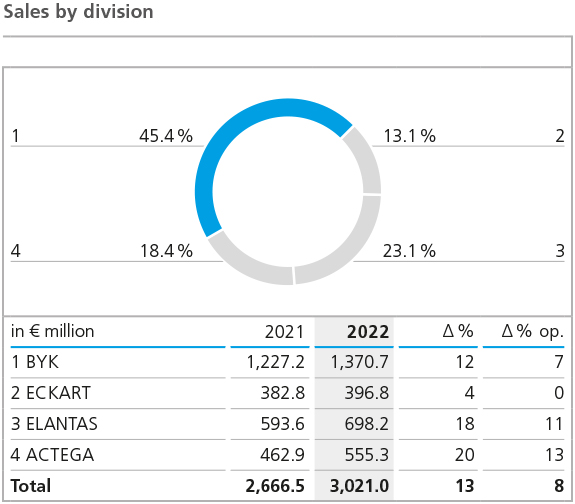

In the 2022 fiscal year, sales in the BYK division increased by 12 % or € 143.4 million to € 1,370.7 million (previous year: € 1,227.2 million). This figure included positive exchange-rate effects of € 60.4 million. Adjusted for this effect, operating sales were 7 % higher than in the previous year.

The external factors of influence in 2022 described above were reflected in the division’s sales performance. The gloomier markets led to significant volume declines, particularly in the second half of the year. However, benefiting from extensive price adjustments as a result of sharp price increases for raw materials, energy, and logistics services, and a good order situation in the first months of the year, satisfactory sales growth was achieved throughout the reporting period. While growth in the Paints and Plastics business lines slowed somewhat, some of the other product lines achieved significant double-digit growth rates.

The regional sales development in 2022 was less uniform than in the previous year. In Europe, it was mainly impacted by the war against Ukraine and in China by subdued demand. The Americas replaced Europe as the region with the highest sales, exhibiting clear double-digit growth even after adjusting for positive exchange-rate effects. The leading market overall was the U.S., followed by Brazil, Mexico, Canada, and the countries of Latin America. Asia continued to develop positively, although growth after exchange-rate adjustments was only in the low single digits. China, which has always been the leading sales market in terms of momentum in recent years, suffered mid-single-digit percentage sales losses after adjusting for exchange-rate effects. This was offset by an extremely positive sales performance in India as well as in other countries in Southeast Asia and the Middle East. In 2022, Europe fell slightly behind the Americas and Asia, remaining at around the prior-year level in nominal and exchange rate-adjusted terms. This was due on the one hand to the economic consequences of the war against Ukraine. On the other, energy price developments in Europe led to a generally dimmed macroeconomic trend. The countries of the European Union, with Germany boasting the highest sales, achieved overall operating growth in the mid-single-digit percentage range. The strongest growth rates were reported in Turkey and Poland.

Sales Performance of ECKART

The ECKART division generated sales of € 396.8 million in 2022 (previous year: € 382.8 million). The year-over-year increase of 4 % was positively influenced by exchange-rate effects as well as by the acquisition of the business activities of TLS Technik GmbH & Co. Spezialpulver KG in Bitterfeld in February 2021. Adjusted for these effects, operating sales were at the previous year’s level. The external factors described above also impacted sales momentum in the ECKART division. The drop in demand was offset by price adjustments to compensate for cost increases in the raw material, logistics, and energy sectors.

Sales development in 2022 was mixed at regional level. The war against Ukraine and the associated energy price development in Europe gave rise to an operating sales decline in almost all countries in which ECKART has a presence. Asia achieved significant operating growth in some markets, such as India. However, as China, the region’s strongest market in terms of sales, recorded a significant decline in operating sales, growth for the region as a whole could only be maintained at a low single-digit level. The region with the greatest sales momentum was the Americas. In the U.S., the strongest sales market in the region, double-digit growth was achieved after adjusting for foreign exchange, and Canada and Brazil also showed strong double-digit growth rates. Only Mexico saw a decline in sales after adjusting for exchange-rate effects. Overall, the region showed growth in the lower double-digit percentage range.

Sales Performance of ELANTAS

In the ELANTAS division, sales increased in 2022 by 18 % or € 104.5 million to € 698.2 million (previous year: € 593.6 million). Operating sales growth, adjusted for positive currency effects, was 11 %. ELANTAS achieved this positive sales growth despite the burdens of the cyclical decline in demand by making inflation-related price adjustments across all product lines.

A look at the regions also shows a deviation in this division compared to the previous year and the consequences of external influencing factors. China, the single market with the highest sales, lost significant momentum here in 2022 and experienced a slight sales drop after adjusting for exchange rates. Overall, however, Asia posted slight sales growth, primarily due to strong growth in the second-largest market, India. Although this division also suffered sales losses in Europe as a result of the sanctions imposed due to the war against Ukraine, it achieved double-digit growth across almost all countries adjusting for exchange-rate influences. The ELANTAS division also recorded its highest operating sales growth in the Americas. Significant sales increases were achieved across all countries. Canada achieved middouble-digit percentage sales growth, and the U.S., the strongest market in terms of sales, also showed high growth rates, followed by Mexico.

Sales Performance of ACTEGA

With sales of € 555.3 million (previous year: € 462.9 million), the ACTEGA division achieved growth of 20 % compared to 2021. Adjusted for positive currency and acquisition effects totaling € 9.8 million due to the acquisition of Henkel’s closure materials business, which was completed back in 2021, the division recorded operational growth of 13 %. This was mainly attributable to price adjustments across all product lines. Operating volume development was slightly negative.

The division’s sales performance in 2022 was positive across all regions. Europe, the region with the highest sales, posted double-digit operating growth despite the economic impact of the war against Ukraine. The Eurozone showed very good momentum with 15 % operating growth. Germany, the largest single market, also performed well boasting a double-digit growth rate. Asia recorded the strongest percentage increase in sales. Deviating from the development in the other divisions, ACTEGA achieved double-digit operational growth in China. The highest percentage increase in operating sales performance was achieved in India. In the Americas, Mexico, followed by Brazil, showed the strongest percentage increase in sales in operating terms. In the U.S., however, the division’s largest single market, ACTEGA achieved only moderate operating growth in the low singledigit range. Overall, sales in the region increased in the double-digit range, driven by strong sales growth in Brazil, but fell slightly short of the other regions.

Earnings Situation

The general slowdown in demand was also reflected in ALTANA’s earnings situation. However, comprehensive price adjustments, in particular to compensate for the significant increase in material, energy, and logistics costs, contributed to the fact that absolute earnings before interest, taxes, depreciation and amortization (EBITDA) fell by only 6 % or € 29.5 million to € 452.2 million (previous year: € 481.7 million). Adjusted for acquisition and exchange-rate effects, operating earnings decreased by 10 %. At 15.0 %, the EBITDA margin was below the previous year’s figure of 18.1 % and below our strategic target range of 18 % to 20 %. The deviation was mainly due to inflation.

The subdued order situation due to external influences and the inflation-related development of costs and sales resulted in an absolute EBITDA and an EBITDA margin below the figures forecast for 2022 at the beginning of the year.

The most important cost parameter for ALTANA, variable raw-material and packaging costs, consistently weighed on earnings development. The material usage ratio, the ratio of these costs to sales, was already at 48.1 % in the first quarter and rose continuously over the course of the year as raw material prices continued to rise, reaching 49.6 % in the fourth quarter. For 2022 as a whole, the material usage ratio was 48.9 %, significantly higher than the prior-year figure of 45.4 % and far higher than we had forecast. At the beginning of the year, we still expected raw material prices to move laterally in 2022. The increase in material costs and the resulting impact on earnings affected all four divisions.

The development of costs in 2022 was mainly influenced by inflation-related price developments in the area of energy, logistics, and other services. In addition, cost items in the area of travel activities rose to a higher level again following the discontinuation of many restrictions due to the coronavirus pandemic. Depreciation and amortization increased by 4 % in a year-to-year comparison. Personnel costs were impacted by a further increase in the number of jobs, mainly in production, and annual pay increases. The ratio of total personnel costs to sales fell to 19.7 % (previous year: 20.9 %) due to the increase in sales.

Within production costs, personnel costs in particular were higher than in the previous year due to the increase in personnel to safeguard capacity and tariff adjustments. The second largest effect came from significantly higher energy costs, followed by higher costs for maintenance and repairs.

In terms of selling expenses, the main driver for 2022 was the increase in freight prices, which accounted for around half of the cost increase. The second-largest effect here was the increase in personnel expenses, mainly due to collective pay increases and the expansion of the workforce to safeguard business operations. In the area of selling expenses, the elimination of travel restrictions also led to an increase in the corresponding cost items.

In 2022, research and development expenses rose again. The reason for the increase was personnel costs as well as an increase in travel expenses. The ratio of research and development costs to total sales decreased slightly from 6.7 % to 6.4 % due to the high sales growth in 2022 and is thus slightly below our target of around 7 %.

Administrative expenses also increased vis-à-vis the previous year. Here, too, the main reasons were increases in personnel expenses, increases in IT consulting costs, and higher travel expenses. However, the ratio of administrative expenses to sales remained at the prior-year level of 4.4 %.

The positive balance of other operating income and expenses totaled € 8.5 million in 2022, slightly below the previous year’s figure (€ 10.4 million). Earnings before interest and taxes (EBIT) amounted to € 287.5 million, 14.5 % lower in operational terms than the previous year’s figure (€ 322.8 million).

At € 7.0 million, the financial result was higher than the previous year’s figure of € - 2.0 million. The positive result was mainly based on the income from the sale of the shares in the company dp polar GmbH, Eggenstein-Leopoldshafen, which was previously accounted for using the equity method, in October 2022. The result from companies accounted for using the equity method changed from € - 45.8 million in the previous year to € 10.9 million in the 2022 fiscal year. The reason for this development is valuation effects in connection with the investment in Landa Corporation Ltd. As a result of several capital increases, ALTANA’s share in the company decreased while the proportionate equity increased significantly.

Earnings before taxes (EBT) increased to € 305.5 million (previous year: € 275.0 million), while earnings after taxes (EAT) rose to € 232.4 million (previous year: € 195.2 million). The adjusted income tax rate was slightly lower than in the previous year.

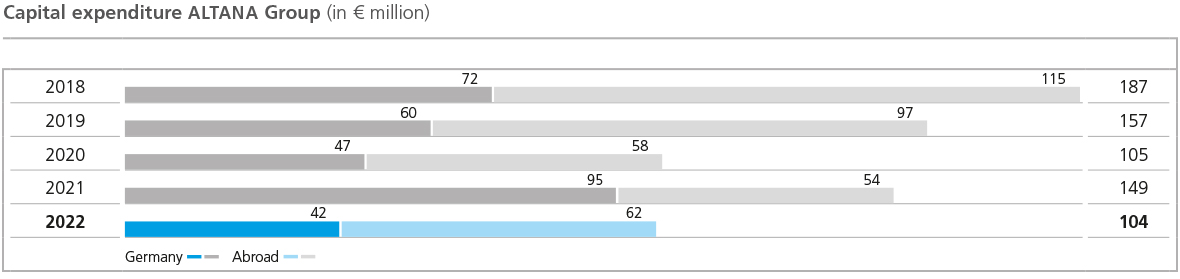

In the past fiscal year, ALTANA invested a total of € 103.5 million in intangible assets and property, plant and equipment, which was below the prior-year figure (€ 149.3 million). In 2021, € 46.3 million was spent on acquiring intangible assets and property, plant and equipment in connection with the acquisition of business activities in the ACTEGA division. Total investments adjusted for this acquisition amounted to € 103.0 million. The investment ratio, that is the ratio of capital expenditures to sales, was 3.4 %, below our long-term target range of 5 % to 6 % due to inflationrelated sales growth.

Of the € 103.5 million invested, € 95.0 million related to property, plant and equipment (previous year: € 93.5 million). For several years, major projects have been carried out to strategically expand global production and laboratory capacities. Investments in intangible assets totaled € 8.5 million in the past fiscal year, compared to € 9.5 million in 2021. The focus of investments was on the further expansion of digitization and ERP systems.

In the regional distribution of investments, there was a project-related shift in favor of the Americas compared with the previous year. While Europe’s share decreased from 61 % in 2021 to 56 % in the reporting year, the Americas’ share grew to 34 % (previous year: 27 %). The increase was mainly due to investment projects in Brazil. Overall, investment activity continued to be focused on Germany (41 %) and the U.S. (28 %). Asia’s share of the total volume decreased to 10 % (previous year: 12 %).

The BYK division invested a total of € 41.5 million in 2022, slightly below the previous year’s level (€ 42.6 million). Investment activity focused on the further expansion of production capacities in the U.S. and Germany. Other investments concerned research and development capacities as well as strategic digitization projects.

At € 22.3 million, the ECKART division’s investment volume was lower than in the previous year (€ 24.9 million). As in the prior year, the division’s site in Hartenstein and its sites in the United States accounted for by far the largest shares.

The ELANTAS division increased its investments in property, plant and equipment and intangible assets to € 16.4 million (previous year: € 11.5 million). In the past fiscal year, the division invested primarily in the production facilities of its European companies and its site in Zhuhai, China.

The ACTEGA division increased its investment volume to € 20.7 million (previous year: € 18.9 million). Investments in the past fiscal year mainly related to the expansion of production capacities at German sites and at its site in Brazil.

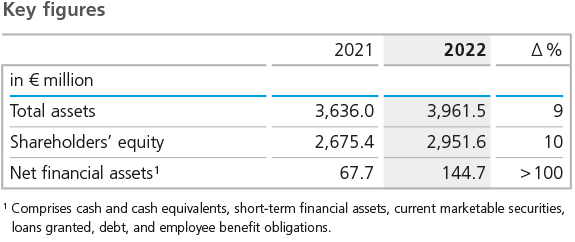

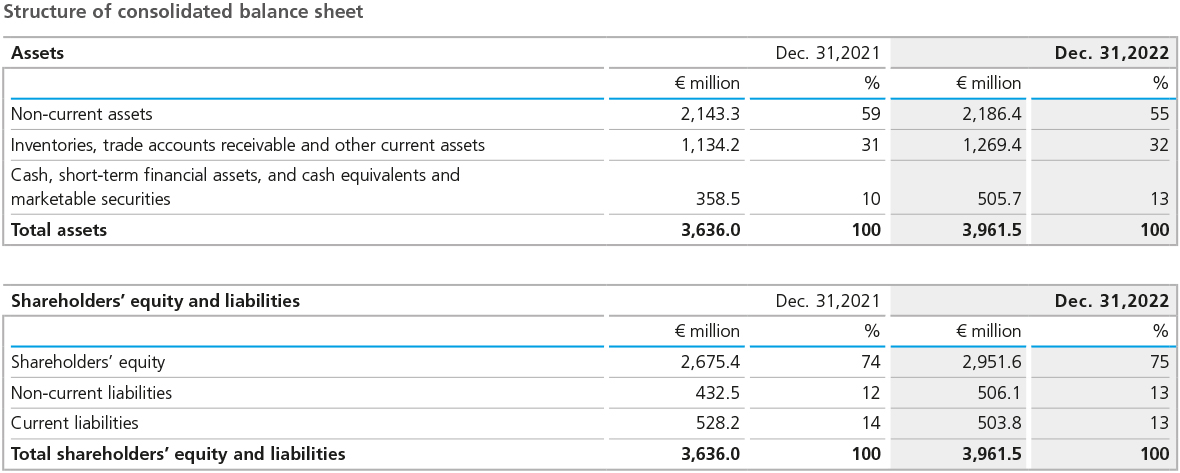

In the course of the 2022 fiscal year, the ALTANA Group’s total assets rose from € 3,636.0 million to € 3,961.5 million. The increase of € 325.5 million or 9 % results primarily from an increase in current assets due to an increase in inventories and cash and cash equivalents as well as from exchange-rate effects.

Intangible assets decreased to € 986.2 million (previous year: € 995.4 million). Property, plant and equipment increased slightly in value, developing from € 997.9 million in the previous year to € 1,012.3 million. With additions of € 95.0 million, the level of investment in property, plant and equipment was below that of depreciation and amortization. Positive exchange-rate effects contributed to an increase in the carrying amounts in the Group currency, the euro, in both areas.

Shares in companies accounted for using the equity method increased by € 36.3 million to € 83.6 million. The rise was mainly due to an increase in this item resulting from the change in the shareholding structure of Landa Corporation Ltd. in the course of several capital increases.

Total non-current assets amounted to € 2,186.4 million at the balance sheet date (previous year: € 2,143.3 million), up € 43.1 million on the previous year. Their share of total assets decreased to 55 % (previous year: 59 %).

The change in current assets was mainly due to the increase in inventories and cash and cash equivalents. The value of inventories and trade accounts receivable increased as a result of inflation-related price increases and exchangerate effects. Inventories were also boosted by the build-up of raw material stocks in the wake of continuous price increases and limited availability, with demand increasingly weakening in the second half of the year. Inventories increased to € 616.5 million (previous year: € 511.5 million). At € 487.6 million, trade receivables were higher than in the previous year (€ 473.4 million). As a result of these effects and a simultaneous reduction in trade payables, net working capital was significantly higher in absolute terms than in the previous year. In the balance with current liabilities, net working capital, at € 871.8 million, was well above the level of 2021 (€ 737.1 million). The scope of net working capital, in relation to the business performance of the respective preceding three months, rose to 138 days, compared with 118 days at the end of 2021. Absolute net working capital as well as the scope were also higher than the figures expected for 2022, as neither inflation-related price increases nor exchange-rate and demand developments were forecast in this way at the beginning of the year. Cash and cash equivalents increased in the course of the year to € 458.1 million (previous year: € 259.9 million), mainly due to the inflow from non-current financial liabilities. Based on these effects, total current assets climbed to € 1,775.0 million (previous year: € 1,492.7 million).

On the liabilities side, changes resulted primarily from earnings-related increases in equity, increases in non-current financial liabilities, a reduction in pension provisions, and exchange rate-related adjustments. The Group’s equity improved overall by € 276.2 million or 10 % to € 2,951.6 million (previous year: € 2,675.4 million). The positive result for the year as well as currency and pension valuation effects were the main contributory factors. At 75 %, the equity ratio as of December 31, 2022, was slightly above the previous year’s level.

Total non-current liabilities increased in the course of 2022, mainly due to the utilization of a credit line from the European Investment Bank (EIB), while provisions for pensions decreased, mainly as a result of interest rates. Overall, non-current liabilities increased by € 73.6 million to € 506.1 million (previous year: € 432.5 million).

The total current liabilities reported in the balance sheet as of December 31, 2022, fell from € 528.2 million to € 503.8 million. Trade payables decreased slightly by € 15.6 million to € 232.2 million.

The balance of cash and cash equivalents, short-term financial assets, current marketable securities, loans granted, financial liabilities, and employee benefit obligations resulted in net financial assets of € 144.7 million at the balance sheet date of December 31, 2022. This corresponds to an increase of € 77.0 million compared with the previous year.

Principles and Goals of Our Financing Strategy

We generally aim to finance our operating business activities from the cash flow from operating activities. The same applies to the need for capital expenditure, which caters to the continual expansion of business activities.

As a result, our financing strategy is oriented to keeping the cash and cash equivalents generated within the Group centralized. In addition, a financing framework is sought that enables ALTANA to flexibly and quickly carry out acquisitions and even large investment projects beyond the accustomed scope.

To successfully implement these goals, we manage nearly all of the Group’s internal financing centrally via ALTANA AG. To this end, cash pools are set up for the important currency areas.

In June 2021, ALTANA restructured its long-term Group financing: Since June 2021, ALTANA has had access to € 250.0 million in the form of a syndicated credit facility from an international bank consortium which has a minimum term until 2026. In 2022, the term was extended until 2027. In addition, ALTANA has had access to loans from the European Investment Bank (EIB) of up to € 200.0 million since the end of June 2021 for the development of climate-friendly, digital, and sustainable products. In the 2022 fiscal year, the EIB loan commitment was increased by € 50 million to a total of € 250 million and the call period was extended by one year to December 21, 2023. EIB loans totaling € 150.0 million were drawn down by the end of 2022.

This financing structure offers ALTANA the flexibility it needs to appropriately take advantage of short-term or investment-intensive growth opportunities. The distribution of the maturities of the financing instruments we use enables us to optimally control repayment of liabilities with inflows from operating cash flow.

Off-balance-sheet financing instruments result from bank guarantees, purchasing commitments, and guarantees for pension plans. Details on the existing financing instruments are provided in the complete Consolidated Financial Statements.

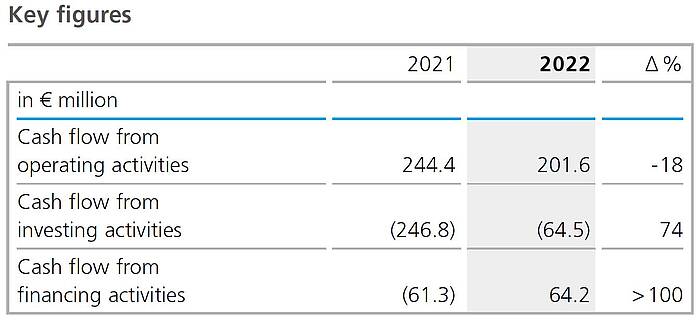

In the course of 2022, cash and cash equivalents increased by € 198.1 million to € 458.1 million (previous year: € 259.9 million). At € 201.6 million, the cash inflow from operating activities was below the previous year’s level (€ 244.4 million) and below our expectations: We had forecast an increase compared to the previous year. This reflects the high level of capital tied up in net working capital, which increased by € 125 million over the course of the year, in particular the sharp rise in inventories.

Cash outflow from investing activities decreased to € 64.5 million (previous year: € 246.8 million). One of the main reasons for this was the repayment of current financial assets in 2022, which had represented a cash outflow in the previous year. In contrast to 2021, moreover, no expenditures were made for acquisitions in 2022. Capital expenditure on intangible assets and property, plant and equipment, adjusted for acquisitions, was at roughly the same level as in 2021.

Cash flow from financing activities amounted to € 64.2 million in the 2022 fiscal year, which were mainly provided by drawing down the loan from the European Investment Bank. In the previous year, there was an outflow of funds from financing activities totaling € 61.3 million. In fiscal 2022, ALTANA AG paid a dividend amounting to € 70.0 million (previous year: € 50.0 million).

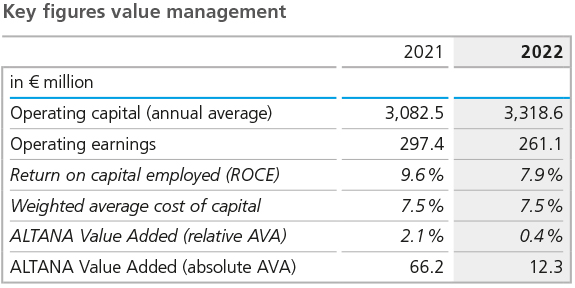

ALTANA determines the change in the company’s value via the key figure ALTANA Value Added (AVA), whose calculation is explained in the “Group Basics” section. In addition, the key figure Return on Capital Employed (ROCE), which is also presented in the “Group Basics” section, is used to measure the development of the company’s value. Despite challenging conditions, a slightly positive contribution to the development of our company’s value was generated in the 2022 fiscal year, although this was lower than the very good figure for the previous year and also well below our expectations for the fiscal year.

The earnings development is reflected in the operating earnings of € 261.1 million (previous year: € 297.4 million), which was the main factor here. The Group’s average capital employed increased to € 3,318.6 million in 2022 (previous year: € 3,082.5 million). The cost of capital rate remained unchanged at 7.5 %, resulting in costs of capital of € 248.9 million (previous year: € 231.2 million).

At 7.9 %, the return on capital employed (ROCE) in 2022 was down on the previous year (9.6 %). Absolute value added totaled € 12.3 million in the past fiscal year, compared to € 66.2 million the year before. Relative AVA fell from 2.1 % in the previous year to 0.4 % in 2022. The significant increase in the value management key figures originally forecast for 2022 was not achieved due to the earnings situation, which was adversely affected by the external environment.